Find the right drink driving solicitor for your case

Driving under the influence of alcohol is a serious offence in the UK, and has severe penalties for those convicted including fines and driving disqualifications. If you find yourself facing a drink driving charge, it is essential to seek legal representation to navigate through the complex legal system and protect your rights.

Finding the right drink driving solicitor can make a significant difference in the outcome, here’s how to find the right one for you and your case.

The role of a drink driving solicitor

When charged with a drink driving offence, it can be overwhelming to know where to turn for help. This is where a drink driving solicitor comes in. They are legal professionals with the knowledge and expertise to guide you through the legal process and ensure your rights are protected.

What does a drink driving solicitor do?

A drink driving solicitor‘s primary role is to provide legal representation and advice to individuals facing drink driving charges. They will analyse your case, gather evidence, and build a strong defence strategy tailored to your specific circumstances. They will also guide you through the court proceedings and represent you during hearings, aiming to achieve the best possible outcome.

Why you need a specialist drink driving solicitor

While any solicitor can technically handle drink driving cases, it is wise to choose a specialist solicitor who has experience in dealing specifically with these types of offences.

A specialist drink driving solicitor will be up-to-date with current legislation, know the various defenses that may be applicable to your case, and have a track record of success in similar cases. They will work diligently to protect your interests and minimize the potential consequences of a conviction.

Factors to consider when choosing a drink driving solicitor

Experience and expertise

One of the most crucial factors to consider is the solicitor’s experience and expertise in handling drink driving cases. Look for drink driving solicitors who have successfully represented clients in similar situations and have a solid understanding of the relevant laws and procedures.

Check their track record and ask about their experience with cases that resemble yours. A drink driving solicitor with a proven track record is more likely to provide effective representation and achieve a favourable outcome.

Reputation and reviews

Research the solicitor’s reputation and read reviews or testimonials from previous clients. This will give you an insight into their professionalism, communication skills, and ability to deliver results.

Additionally, consider seeking recommendations from trusted friends or family members who may have gone through similar legal situations. Their firsthand experiences can help you identify reputable drink driving solicitors in your area.

Fees and payment structures

Discuss the fees and payment structures with potential drink driving solicitors before making a decision. While cost shouldn’t be the sole determining factor, it is essential to have a clear understanding of the financial aspects involved.

Some solicitors may offer fixed fee arrangements, while others may charge hourly rates. Clarify what services are included in the fee and whether any additional expenses may arise during the course of your case.

What to expect when working with a drink driving solicitor

Initial consultation

The first step is an initial consultation with your chosen drink driving solicitor. This meeting allows them to assess your case, gather relevant information, and discuss the potential defences available to you.

During the initial consultation, be prepared to provide details about the circumstances surrounding your drink driving offence, any witnesses, and any evidence you may have. This information will help your solicitor build a solid defence strategy.

Building your defence

Based on the information gathered during the initial consultation, your drink driving solicitor will begin building your defence. They will analyse the evidence, identify any weaknesses in the prosecution’s case, and explore possible defences that can be presented in court.

Throughout this process, your solicitor will maintain open lines of communication, keeping you informed about the progress of your case and any developments that may arise.

Court representation

If your case goes to court, your drink driving solicitor will present your defence, cross-examine witnesses, and argue your case in front of the court.

Your solicitor’s expertise in drink driving cases will be crucial during this stage. They will use their knowledge of the law, their understanding of your case, and their experience in court to advocate for your rights and challenge the evidence presented against you.

Avoid a sentence with an experienced drink driving solicitor

Having an inexperienced drink driving solicitor with little knowledge of drink-driving cases could mean you end up with a more severe sentence than you deserve because they don’t explain the mitigating circumstances properly.

Having a quality drink-driving solicitor could be the difference between going to prison and not, or losing your licence and not.

Dispute resolution is a critical aspect of resolving conflicts and disagreements that arise in both personal and professional settings. With a myriad of options available, it can be challenging for individuals and organizations to decide which approach best suits their needs. This article provides an in-depth exploration of three primary dispute resolution methods: mediation, arbitration, and litigation. By understanding the differences between these methods and their respective advantages and disadvantages, you can make an informed decision when faced with a conflict.

1. The Importance of Dispute Resolution

Resolving disputes is essential in maintaining healthy relationships, ensuring smooth business operations, and promoting a peaceful society. Dispute resolution seeks to address conflicts by finding mutually acceptable resolutions that uphold the interests of all parties involved. By engaging in effective dispute resolution, individuals and organizations can prevent minor disagreements from escalating into more significant, costly, or time-consuming issues.

1.1 Conflict Resolution vs. Dispute Resolution

While the terms conflict resolution and dispute resolution are often used interchangeably, they refer to different concepts. Conflict resolution focuses on addressing the underlying causes of a disagreement, such as miscommunication or differing perspectives, to prevent future conflicts from arising. On the other hand, dispute resolution concentrates on resolving the current disagreement through various processes and techniques.

2. Mediation: Facilitating Consensus

Mediation is a flexible and informal method of dispute resolution in which a neutral third-party mediator assists disputing parties in reaching a mutually acceptable agreement. The mediator does not have the authority to impose a decision; instead, they help facilitate communication and negotiation between the parties to identify common ground and devise a satisfactory resolution.

2.1 The Role of the Mediator

The mediator’s primary function is to guide the disputants through a structured dialogue, helping them uncover their underlying interests and concerns. Mediators may work with the parties jointly or separately, adopting various communication techniques and problem-solving strategies to help them develop creative solutions that address their needs.

2.2 Advantages of Mediation

Mediation offers several benefits over other dispute resolution methods:

It encourages open communication and fosters a collaborative problem-solving approach.

It is generally faster and more cost-effective than litigation or arbitration.

It allows parties to maintain control over the outcome, resulting in a voluntary, nonbinding agreement that is more likely to be upheld.

It can preserve relationships by mitigating the adversarial nature of disputes.

3. Arbitration: Binding Decision-Making

Arbitration is a more formal dispute resolution method in which an impartial third-party arbitrator hears the arguments and evidence presented by the disputing parties and renders a binding decision. Arbitration is often viewed as a hybrid between mediation and litigation, offering a structured, yet less adversarial and time-consuming process.

3.1 The Arbitration Process

The arbitration process can be customized to suit the needs and preferences of the disputing parties. They can agree on various aspects, including the presence of legal counsel, the rules of evidence, the timeline, and the selection of the arbitrator. Once the arbitration proceedings commence, both parties present their cases, and the arbitrator considers the arguments and evidence before issuing a decision.

3.2 Advantages of Arbitration

Arbitration offers several benefits over litigation and, in some cases, mediation:

It is generally faster and less expensive than litigation.

It allows for greater flexibility and customization of the process.

The arbitrator’s decision is binding and usually confidential, providing a sense of finality and privacy for the parties involved.

It may be more suitable for complex or technical disputes that require specialized knowledge.

4. Litigation: The Courtroom Battle

Litigation is the most formal and well-known method of dispute resolution, involving a plaintiff and a defendant presenting their cases before a judge or a judge and jury in a court of law. The judge or jury is responsible for weighing the evidence, interpreting the applicable laws, and issuing a legally binding decision.

4.1 The Litigation Process

The litigation process is characterized by a series of stages, including the filing of a complaint, the discovery phase, pretrial motions, and, if necessary, a trial. Throughout the process, lawyers play a significant role in representing their clients, conducting research, and crafting legal arguments. Often, disputes are resolved through settlement agreements during the pretrial phase.

4.2 Advantages of Litigation

While litigation is generally the most time-consuming and costly dispute resolution method, it offers certain advantages:

It provides a definitive, legally binding resolution that can be enforced by the courts.

It is appropriate for disputes where the parties have irreconcilable differences or require a court’s intervention to protect their rights.

The litigation process is governed by established rules and procedures, ensuring a transparent and structured approach to dispute resolution.

5. Choosing the Right Dispute Resolution Method

Selecting the appropriate dispute resolution method depends on various factors, including the nature of the dispute, the parties’ relationship, the desired outcome, and the available resources. By considering the advantages and disadvantages of mediation, arbitration, and litigation, disputants can make informed decisions that best serve their interests.

5.1 Assessing the Dispute

To determine the most suitable dispute resolution method, disputants should first assess the nature of their disagreement. This assessment may include examining the legal and factual complexities, the amount at stake, and the desired remedies. For instance, complex disputes involving technical expertise may be better suited for arbitration, while disputes requiring legal interpretation or precedent-setting decisions may necessitate litigation.

5.2 Evaluating the Parties’ Relationship

The relationship between disputing parties can also be a crucial factor in choosing the right dispute resolution method. For ongoing relationships, such as business partners or family members, mediation may be the preferred option as it provides a less adversarial and more cooperative approach. Conversely, in situations where the relationship has deteriorated beyond repair, litigation may be necessary to protect each party’s rights and ensure a legally binding resolution.

5.3 Weighing the Costs and Benefits

Lastly, disputants should consider the potential costs, benefits, and risks associated with each dispute resolution method. Mediation and arbitration tend to be less expensive and time-consuming than litigation, but they may not be appropriate in all situations. Disputants should carefully weigh the potential outcomes and the likelihood of achieving their desired results through each method before making a decision.

6. The Future of Dispute Resolution

The field of dispute resolution continues to evolve, with new methods and technologies emerging to address the changing needs of disputants. Some examples of recent developments include online dispute resolution (ODR) platforms, which facilitate mediation and arbitration through virtual channels, and hybrid models that combine elements of mediation and arbitration, such as med-arb. As these innovations gain traction, disputants will have even more options to choose from when resolving their conflicts.

7. Key Takeaways

Dispute resolution plays a vital role in addressing conflicts and promoting harmonious relationships in both personal and professional spheres. Understanding the distinctions between mediation, arbitration, and litigation can help disputants make informed decisions about the most appropriate method for their unique circumstances. By selecting the right process, parties can maximize their chances of reaching a satisfactory and lasting resolution to their disagreements.

No one anticipates needing a lawyer, but there may come a time when you need a lawyer at your side, defending your name in front of a judge. If this time ever comes, there are a few things that you need to remember before hiring the right defense lawyer for your case. Keep reading to find some invaluable advice that might come in handy later down the line.

Their Experience

Before agreeing to an interview with the attorney, you should find out about their credentials. You want to know where they went to school, how long they’ve been practicing law, and whether they have experience with your case, whatever that may be. Hiring an inexperienced lawyer will only harm you in the long run, so you must know their history before agreeing to a meeting.

Ask About Their Success Rate

An essential factor to discuss is the potential attorney’s success rate. Do they have a high rate of wins, or do the losses trump the wins? Learning about their success rate is important because you want someone who knows how to perform the job to the best of their ability. After all, your freedom might be on the line, so you want the best person for the job defending you in court.

Trial Cases

Another essential thing to discuss with the potential attorneys is whether they have had many cases go to trial. Most people don’t want to drag their lives through the court system for an extended period. Not wanting to spend their lives in court means that most people don’t want to go to trial, and they’d prefer to settle before that happens. Ask the attorney how often the potential attorney has been to trial and the success rate of their trials before deciding to hire them as your attorney. For a better success rate of trial cases you can refer to an Ottawa criminal defence lawyer.

Do They Appear at the Courthouse Often?

It’s imperative to have an attorney who has a history with the judges in your area, so you want to find out how often they appear in the courthouse where your case will be tried. If they haven’t had many cases in front of the judges in your courthouse, then finding a different attorney would be the best decision.

Will They Be Working on Your Case?

Typically, lawyers work for firms that have several different lawyers working on cases at the same time. Before agreeing to hire a defense attorney, find out if the attorney will be the one who is working on your case or would your case be handed over to someone else. If there are going to be different people working on your file, then you should find an attorney that is capable of giving you his full attention to your case.

How Strong is Your Case?

You should be aware that no matter how strong your case is, there is always a chance that you could lose. There is no guarantee that you will win, even with the best defense attorney at your side. Regardless, it’s essential to find out if you have a strong case, so you don’t waste your valuable time or resources.

No one wants to find themselves standing in front of a judge; that much goes without saying. But if you must go to court, you want to be prepared at the start. This means that you want to have the best defense attorney by your side. If you’re in a position where you need to find a defense attorney, then follow these tips, do your research, and you should have the best attorney for your needs.

Becoming a lawyer is a dream for many, and the bar exam is the first hurdle you need to cross before achieving that dream. The bar exam is one of the most difficult exams to ace with a high failure rate, but you can make sure you pass with flying colors with the right preparation and strategies. To help you prepare, there are a variety of bar prep courses that are available to assist you in your journey towards passing the bar exam. In this article, we will explore the different bar exam prep options, how to create an effective study plan, and tips and strategies for acing the bar exam.

Introduction to Bar Exam Preparation

The US Bar Exam is a grueling test that requires a significant amount of time and dedication to prepare for. It’s important to understand the scope of the exam and how to best prepare for it. Before you begin your bar prep journey, it’s essential to understand the different types of bar exams and the materials you need to master for each.

The most common type of bar exam is the Uniform Bar Exam (UBE). This exam is offered in all 50 states, the District of Columbia, Guam, and the US Virgin Islands. The UBE consists of three components: the Multi-State Bar Exam (MBE), the Multi-State Performance Test (MPT), and the Multi-State Essay Exam (MEE). Each of these components require different types of preparation. The bar exam is typically a two-day exam, but the exact duration varies from state to state. The exam is designed to assess the legal knowledge, skills, and abilities of prospective lawyers, and the pass rate is typically around 60-70%. Therefore, it is important to prepare for the bar exam and ensure that you are well-equipped to tackle the different questions and topics tested on the exam.

In addition to the UBE, some states may require you to take a state-specific portion of the bar exam. This can include a state-specific essay exam or a state-specific multiple-choice exam. It’s important to understand the requirements of your state’s bar exam in order to adequately prepare.

Why You Need A Bar Prep Course

Taking a bar prep course can be a great way to prepare for the bar exam. A bar prep course can help you understand the material and provide structure to your studying. It can also provide tips and feedback on how to improve your performance on the exam.

Some bar prep courses also provide practice tests and materials to help you become more familiar with the legal topics and the exam format. These courses can also provide guidance on the best way to approach the bar exam and the types of questions you can expect to see on the exam.

Finally, taking a bar prep course can help you to stay motivated and on track with your studying. It can provide a sense of community and support, which can be invaluable during the bar exam preparation process.

Benefits of Taking a Bar Prep Course

Taking a bar prep course can provide several benefits for those preparing for the bar exam. First, it can help you develop a better understanding of the material and the exam format. A bar prep course can also provide structure and guidance for your studying.

Second, it can provide practice tests and materials to help you become more familiar with the legal topics and the exam format. Finally, it can provide motivation, support, and accountability to help you stay on track with your studying.

Comparing Different Bar Prep Courses

When choosing a bar prep course, it’s important to compare the different options to determine which one is best for you. There are several factors to consider when comparing bar prep courses, such as the cost, the content, the support offered, and the format.

Some of the most popular bar prep courses include Barbri, Themis, Kaplan, and Studicata. Each of these courses have different features and benefits, so it’s important to compare them to determine which one is best suited for your needs.

Bar Exam Prep Options

There are a few different bar exam prep options available to help you prepare for the bar exam. These include self-study, online courses, tutoring, and bar review courses.

Self-study is the most affordable option and allows you to create your own study plan, but it can also be more difficult and time-consuming. Online courses are a good option for those who want a structured study plan and guidance, and tutoring can provide a personalized approach to studying for the bar exam. Bar review courses are the most comprehensive option and provide the most comprehensive preparation for the bar exam.

Barbri Bar Prep Course

Barbri is one of the most popular bar review courses, and it is designed to help students pass the bar exam. The bar prep course provides an extensive review of the topics tested on the bar exam and offers a variety of tools and resources such as practice questions and essay outlines. The course also provides guidance on how to create a study plan and tips and strategies for acing the bar exam.

The course is divided into two sections: the MBE review and the state-specific review. The MBE review consists of two full-length practice exams and provides an in-depth analysis of all the topics tested on the MBE. The state-specific review covers the topics tested on the state-specific portion of the bar exam and provides practice questions and essay outlines.

Kaplan Bar Prep Course

Kaplan is another popular bar review course that provides an extensive review of the topics tested on the bar exam. The course is divided into two parts: the MBE review and the state-specific review. The MBE review provides an in-depth analysis of all the topics tested on the MBE, and the state-specific review covers the topics tested on the state-specific portion of the bar exam.

The course also provides practice questions and essays, and it offers a variety of tools and resources such as practice exams and study plans. The course is designed to help students pass the bar exam and provides tips and strategies for acing the bar exam.

Themis Bar Prep Course

Themis is another bar review course that provides an extensive review of the topics tested on the bar exam. The course is divided into two parts: the MBE review and the state-specific review. The MBE review provides an in-depth analysis of all the topics tested on the MBE, and the state-specific review covers the topics tested on the state-specific portion of the bar exam.

Themis also provides practice questions and essays, and it offers a variety of tools and resources such as practice exams and study plans. The course is designed to help students pass the bar exam and provides tips and strategies for acing the bar exam.

Studicata Bar Prep Course

Studicata is another bar review course that provides an extensive review of the topics tested on the bar exam. The course is divided into two parts: the MBE review and the state-specific review. The MBE review provides an in-depth analysis of all the topics tested on the MBE, and the state-specific review covers the topics tested on the state-specific portion of the bar exam.

The course also provides practice questions and essays, and it offers a variety of tools and resources such as practice exams and study plans. The course is designed to help students pass the bar exam and provides tips and strategies for acing the bar exam.

Creating a Bar Exam Study Plan

Creating an effective bar exam study plan is essential for success on the bar exam. The best way to create a study plan is to break it down into smaller chunks and focus on one topic at a time. You should also create a schedule and set aside specific times for studying and review.

You should also create a list of the topics that need to be covered and prioritize the topics that are most important. You should also set aside time for practice questions and essay outlines, as these are key components of passing the bar exam. Lastly, it is important to create a plan for how you will review the material, as this will help you retain the material and ensure you are prepared for the bar exam.

Tips and Strategies for Acing the Bar Exam

Passing the bar exam is no easy task. It requires dedication and hard work. Here are a few tips to help you successfully pass the bar exam:

First, it is important to create a study plan and stick to it. Make sure you set aside specific times for studying and review, and prioritize the topics that are most important. You should also create a list of the topics that need to be covered and make sure you are thorough when reviewing them.

Second, practice as much as possible. Practice questions and essay outlines are key components of passing the bar exam, and it is important to spend time on them. You should also set aside time for timed practice exams, as this will give you an idea of how you will perform on the actual exam.

Third, it is important to take care of your physical and mental health. Make sure you are getting enough sleep, eating well, and exercising. You should also make sure to take breaks and give yourself time to relax and unwind.

Fourth, you should make sure you are familiar with the format and structure of the bar exam. You should also familiarize yourself with the types of questions that are typically asked on the bar exam, as this will help you prepare for the exam.

Lastly, make sure you have a support system in place. You should have a study group or someone who you can turn to for support and advice. This can be a great source of motivation and can help you stay on track and stay focused.

Resources to Aid Your Bar Exam Prep

There are a variety of resources available to help you prepare for the bar exam. These include books, online courses, tutoring, and bar review courses.

Books are a great way to get an overview of the topics tested on the bar exam, and they provide a comprehensive review of the material. Online courses are a great way to get a structured study plan and guidance, and they provide practice questions and essay outlines. Tutoring can provide a personalized approach to studying for the bar exam, and bar review courses are the most comprehensive option and provide the most comprehensive preparation for the bar exam.

Conclusion

The US Bar Exam is a difficult exam to pass. Taking a bar prep course can be a great way to prepare for the bar exam and increase your chances of success. Barbri is one of the most popular bar prep courses. It offers a comprehensive course that covers all three components of the bar exam and provides a variety of materials and resources to support your studying.

Barbri, Kaplan, Themis, and Studicata are popular bar review courses that provide an extensive review of the topics tested on the bar exam. These courses are designed to help students pass the bar exam and provide a variety of tools and resources to aid in the preparation process. With the right preparation and strategies, you can make sure you pass the bar exam with flying colors.

When preparing for the bar exam, it’s important to set realistic goals and create a study plan. Additionally, it’s important to take advantage of the practice tests and online resources offered by your bar prep course. Finally, it’s important to stay organized and focused while studying for the bar exam.

For this featured interview, based on his experience of more than 3000 cases of medical malpractice, we asked Rodney “What have been the most common difficulties experienced by the legal profession when it comes to running cases of medical negligence/malpractice and how can these be overcome?”

Rodney identified ten themes he has noted over the years, which can catch out even the most experienced lawyers and he went on to discuss each in turn.

Screening

As defence organisations point out, only one in five complaints about possible medical negligence have a likelihood of success and this has been borne out in his own practical experience. It is, therefore, necessary to triage or screen cases at the outset, to make sure that they at least have the potential for being able to display the essential triad of duty of care, breach of that duty, and consequential, or but for, damage. Some cases may appear obvious on face value but as most lawyers have limited medical knowledge, it is important to obtain a preliminary screening report by a medical expert to identify exactly who had the duty of care, what standard should be applied, and whether or not any damage is likely to have occurred specifically because of any suggested breach. This initial opinion can usually be based on a detailed statement from the client but may require the perusal of specific notes and records.

In many cases, the client’s concerns are in fact more in the nature of a complaint about behavioural issues, including the attitude of staff, poor communication skills, or delays in managing their case. These are not within the legal definition of medical negligence or malpractice and are more appropriately handled through the normal complaints procedure for the practice or institution involved, rarely proceeding to litigation. Such complaints usually produce a written response within a matter of months.

On occasions, a hospital or other source may have instigated Serious Incident Review which may identify areas where medical care has been deemed sub-standard and could be subject to a legal challenge. However, if lawyers become involved before such reviews are carried out, it is likely the report would not be released to the client as the matter would be deemed sub-judice.

A secondary review may also be appropriate once the medical evidence is complete. This considers all available evidence and allows the medical expert to work with counsel/ trial lawyers to consider the implications of potential strengths and weaknesses in the case before court proceedings.

Screening helps to contain costs by providing an early general overview of a case, for a fraction of the fees which would be required for a full liability and causation report plus a condition and prognosis report. Too often, Rodney says, he has noted lawyers skipping this vital preliminary phase and proceeding to obtain full reports which require considerable time, effort and for which costs which may not be recoverable.

Finally, he points out that the word ‘SCREENING’ is an excellent acronym for the other nine areas where difficulties can and do arise.

Statute

Almost all jurisdictions have a statute that limits the time allowed for the initiation of a case, usually to between one and five years. This is based on the date the cause of action accrued, modified by circumstances such as the time when the client is judged to have had reasonable knowledge of what has happened, related to age, for instance allowing young persons to bring cases from childhood after their age of emancipation and sometimes for those with mental health issues. Allowing the use of such a statute in defence of a claim is normally within the discretionary power of the court. Therefore, it is important to make sure there is no time bar or, in the alternative, there is a reasonable chance a court will allow proceedings to continue.

The presence of such a statute also serves as a warning to lawyers they should avoid any unnecessary delay in moving forward with their investigations or they may unintentionally run out of time and find themselves on the receiving end of a claim in professional negligence. This is another benefit from swift, initial screening which allows a determination to be made whether or not matters are likely to progress, issuing a holding writ if necessary. If not, the client can be informed, allowing them the latitude to seek other medical or legal advice should they wish before they run out of time.

Counsel

Counsel/Trial Lawyers should be consulted early after the initial screening. As well as giving legal direction for the proceedings, receipt of the screening report allows a more informed discussion of the case, particularly in the raising of particular questions they wish to be included in the briefing of experts. Counsel should maintain an ongoing overview as the various reports are received, to ensure the case stays on track and giving advice on handling any new issues as they arise.

Reports

The initial screening report should give advice on which specialties should be involved and in what order reports should be obtained. Under normal circumstances, the initial report is likely to deal with liability and causation. However, occasionally it is more appropriate to have a report detailing the likely consequential damages which may have arisen as, if these cannot be determined, a report on liability and causation is likely to be superfluous. A subsequence is not the same as consequence and just because a client has a particular complaint does not mean that it is in any way related to a breach of the duty of care. As an example, some weakness in a wrist following a well-healed fracture of the scaphoid bone is more a consequence of the injury even if it could be established the fracture was not fully stabilised for a week after the incident. Many cases fail on causation and, unless this is clear, there is no point in obtaining expert reports to deal with the nature of the injury, the present condition, or likely prognosis.

A duty of care is usually easy to determine. However, sometimes it is not so obvious and a case in medical negligence may be considered against a particular Consultant or Attending when a closer examination would reveal it is actually in the remit of other professionals from different medical specialities or, indeed, para-medical specialities such as nursing or physiotherapy. It is important therefore reports identify and focus on the key issues in the case and clearly elucidates if more than one speciality group has potentially breached their duty of care, such as a General Practitioner, Accident, and Emergency doctor, or other staff, all of whom may need to be co-joined.

Expert

Eminence is not the same as expertise and just because someone is well-known in their profession or has appeared in other cases, does not mean they are appropriate for the subject under discussion. Further, they may not have expertise in writing medical-legal reports, having meetings to negotiate with other experts, or giving evidence in court.

Experts must be chosen wisely, clearly understand their primary duty is to the court no matter who instructs them, and be a recognised expert in the subject matter of the case. They must be able to reason logically, both orally and on paper without using hyperbole, in a way which laypersons in general, and the court in particular, can understand and interpret. They need to be coldly objective and demonstrate no conflict of interest or bias on behalf of the plaintiff, the defence, or a specific line of medical therapy. It is quite reasonable for an expert to advocate a particular view as to how they feel a case should be managed, however, they must also be prepared to accept the fact that there is liable to be a reasonably held range of opinion which they should also state and, if necessary, indicate by logical argument why their opinion should be given preference.

Finally, experts have to accept that the standard is reasonableness, not perfection, and be prepared to alter their stated opinion if new evidence, which they have not previously considered, is presented during proceedings.

Expectations of the client

In some case, especially when the consequences have been devastating for the plaintiff, even the most experienced lawyers may become emotionally involved. The rule is empathy, not sympathy and to remain objective throughout so clear, unencumbered, professional advice may be given to the client. At an early stage, it is necessary to have an in-depth conversation with the client in order to ascertain exactly what outcome they expect from the case. Some want to punish, others wish for monetary compensation but on many occasions the client is primarily looking for a detailed, understandable explanation as to what happened. Anger is a common emotion that is best handled through empathy, understanding, and certainty they are being listened to, rather than any logical argument. Managing a client’s expectations is therefore one of the most important functions of a lawyer and vital if the client is to feel content with the outcome, however long the process takes.

Notes and records

Guided by the initial screening and comments of Counsel, all appropriate notes and records need to be expeditiously sourced, ordered, and paginated for ease of reference especially as, in some cases, many thousands of pages may be involved. As well as contemporaneous medical notes, other records may be valuable, for instance, letters to the client from an institution following a complaint or other internal documents such as a report resulting from a serious incident review. External documents may be available following a post-mortem or inquest and the client themselves may have notes in a diary or even photographs on their phone.

Medical experts should be suspicious if they find notes have been redacted, especially if this has been carried out by the legal team either for the defence or the plaintiff. Unless the redaction relates to the names of third parties, it is not best practice to edit the notes in any way before forwarding them to an expert.

Insurance

Medical-legal cases can be very expensive and costs need to be controlled. There is no such this as a water-tight case and loss can result in a heavy financial burden. Any law firm should be clear about how they are going to be compensated in the event a case does not proceed. Unfortunately, not doing so has led to a number of cases being pursued long after they should have been discontinued, taking proceedings up to the door of the court in order to try and get a settlement of some sort to at least cover expenses. This sort of behaviour is frowned upon by the court system and is bordering on unethical.

Some form of insurance is therefore valuable and in some cases, the client can self-insure or have a legal policy in place to at least cover initial advices. It may also be possible to obtain After the Event Insurance if it is clear from the initial reports and the opinion of Counsel the case has a high likelihood of success. Using a blunderbuss approach, ordering multiple expert reports at an early stage, and even obtaining second reports when one expert report does not appear to back the client’s case is a recipe for financial disaster. Once again, a process or system for conducting medico-legal cases is vital to success, remembering that a “system” is there to Save, Yourself, Stress, Time, Energy, and Money.

No medical knowledge/experience

Rodney points out his credo is “to help clients, their legal advisors and the courts to understand more clearly the nature of medical evidence in individual cases so they can make better decisions.” This should be a fundamental belief for all of those preparing expert reports. Courts make determinations, experts assist by rendering the medical evidence understandable for a lay audience and by giving advice as to acceptable standards of care.

The lawyers most likely to get into trouble with the process are those who do not undertake these proceedings on a regular basis. There are many nuances from both a medical and legal point of view that can make cases that look similar produce markedly different outcomes. One of those is an understanding that perfection is not a reasonable standard and secondly that no medical treatment can be guaranteed success. Known complications arise which is the purpose of the doctrine of informed consent. However, it is also true, that just because a patient has been told about the potential risks associated with a particular therapy or procedure, does not mean that when such difficulties arise it could not be considered due to a negligent act. It very much depends on context and circumstances in the individual case and again the expert should be in the best position to determine whether a poor outcome would reasonably be regarded as due to a known complication in all the circumstances or represent a negligent breach of the duty of care.

In circumstances where experts differ in the interpretation of an objective finding, it is for the courts to assess all the evidence before them and make a determination. Sometimes this is difficult for lawyers to understand and particularly if they lack medical knowledge and experience of such cases. Especially at an early stage in their career, it is good practice to have coaches and mentors both within and outside their firm or even the profession. By reflecting on more challenging cases, they can continue to get the learning from them which in turn grows their expertise in what is a niche area and helps to professionalise their practice.

Guiding/directing an expert

It is an expert’s duty to remain independent and objective, no matter who engages them. It is certainly reasonable to ask questions as to why they have come to a particular conclusion or to ask for an evaluation of new evidence, but it is not acceptable to ask an expert to ‘tweak’ a report in order to place a client in a better light. While some lawyers attempt to justify this by stating they are only trying to do their best for the client, they do not serve either the justice system or their profession well. An expert who agrees to change any element of a report under such circumstances is compromised, not just for that case but for any other, and is open to being severely criticised in court. It is not unknown for experts found to have breached this code of conduct to have their professional registration to practice removed by their governing body. Such censure can have considerable implications for their personal, professional, and financial well-being.

Conclusion

In reflecting on the most frequent challenges he has come across in his three decades of dealing with personal injury and medical malpractice cases, Rodney concludes that representing clients in cases of potential medical negligence requires legal representatives to have an understanding of the many complexities involved and to be aware of the pitfalls. Securing early and proficient advice from an appropriate medical expert can mitigate the financial and reputational risks.

It is clear why Rodney is regarded as one of the foremost authorities on the medical aspects of medico-legal practice, and why his keynote speaking, coaching, and tutoring is so highly regarded by lawyers and doctors involved in such cases.

I am a forensic psychiatrist with experience and expertise in correctional health care administration and clinical practice. My area of expertise is suicide and wrongful death in jails and prisons. By researching and analyzing risk factors of suicide and developing prevention strategies, I have established considerable expertise in the field. As a consultant, I provide expert opinions and, if reasonable medical opinion, testimony on disputes such as standard of care, deliberate indifference, and civil rights violations. I have consulted on at least 70 cases under litigation in the United States and testified in at least 20 cases.

Introduction

During the last forty years, courts have attempted to address issues about legal liability related to suicide. The decisions cover various practices in jails and prisons, including diagnosis, monitoring, treatment, communication, policies, staffing, and training.

1 Inadequacy of mental health evaluation

In Comstock v. Mc Crary(1), psychologist Mc Crary did not perform an adequate psychological evaluation and risk assessment of an inmate who committed suicide. Had he done a detailed psychological evaluation, he would have known that several enemies who called him a snitch bothered the decedent.

2 Failure to identify obvious and substantial risk factors

In Williams v. Mehra (2), the significant issue involved a failure to identify an inmate’s substantial risk factors, including depression, psychiatric hospitalization, suicide ideation, and a previous suicide attempt with antidepressant tablets. The psychiatrists neglected to review the record that contained his diagnosis, suicidality, and specific treatment measure to address his suicidality, i.e., prescribing liquid medication. Also, procedurally, the nurse failed to manage his medication on a watch take basis.

3 Psychotropic medication practice

In Greason V. Kemp, (3), the Court held abrupt discontinuation of psychotropic medications of an inmate with a recent history of suicide attempts constituted deliberate indifference. Greason killed himself in a Georgia prison. A doctor abruptly discontinued his antidepressant medication without reviewing his clinical file, conducting a mental status examination, or ordering close monitoring. The Court identified the department’s failure to train the staff, inadequate mental health care delivery, and delayed or denied treatment.

In Steele v. Shah, (4), a psychiatrist discontinued Steele’s psychiatric medications. Steele had a long history of depression, drug addiction, and attempted suicide twice before starting his long sentence. The district court granted the psychiatrist’s motion for a summary judgment, indicating that his decision was nothing more than a disputed medical opinion. On appeal, the 11th Circuit held that “psychiatric needs can constitute serious medical needs and that the quality of psychiatric care one receives can be so substantial a deviation from the accepted standards as to evidence deliberate indifference to serious psychiatric needs.”

4 Officers’ failure to communicate an arrestee’s suicide statements

In Gordon V. Kidd (5), the Court established that failure by an arresting officer to communicate to booking officers constitutes deliberate indifference.

In Conn v. City of Reno, (6) the Court of appeals reversed a district court’s grant of summary judgment in favor of two officers because there was “sufficient evidence to create a genuine fact regarding defendants’ “subjective awareness” of a serious medical need.

In Freedman v. City of Allentown, (7), in contrast to Gordon v. Kidd and Conn v. City of Reno, the Court decided that a probation officer’s knowledge of an arrestee’s previous suicide attempt did not reach the threshold of deliberate indifference when he did not inform the arresting officer. Therefore, his actions were not intentional, malicious, or reckless, and “at most the averments against the officer amount to a lack of due care and are not actionable as a 1983 claim.”

5 Suicidal ideation, suicide watch, and logging

Mental health professionals often release inmates who deny suicidal ideation from suicide watch. Some inmates intentionally conceal their true intentions after they make their decision to exit the world.

In Woodard v. Myres, (8), the claims centered on the failure to institute standard suicide watch, lack of suicide watch monitoring and logging, premature discontinuation of suicide watch, and noncompliance with the facility’s policies and practice.

In Simmons v. Navajo County, (9) the Court opined that placing a pretrial detainee on suicide watch, even the highest level, standing alone “does not demonstrate that an official was subjectively aware of a substantial risk of imminent suicide.” As per Simmons ‘ Court, determinants of imminent suicide risk include “observed suicidal actions, heard statements of suicidal, or witnessed evidence of suicidal intent,” indicating a strong likelihood of suicide.

In Hott v. Minnesota (10), falsification of suicide watch by an officer resulted in an unfavorable court decision for the officer.

In Minix v. Canarecci (11), the district court opined that there was enough evidence to allow a jury to find a direct causal link between the Jail’s practice of classifying and releasing detainees from suicide watch and suicide.

In Broughton v. Premier Health Care Servs., (12), the issue was intentional concealment of suicidal ideation, making it difficult to stake a successful claim against correctional officials. The Court opined, “While Broughton’s disclaimer of suicidal ideation does not automatically insulate the defendants from liability, it does undermine the claim that they willfully ignored his past medical history and current symptomology.”

Strickler V. Mc Cord (13) illustrates the difficulty for jail officials charged with the care of inmates who are determined to commit suicide. The Court found, “He lied on the intake form; he lied when questioned about suicidal thoughts at the Bowen Center, and he deceived the guards about his medication and the razor blades.”

6 Recent Suicide attempt and failure to get prior medical records.

A recent suicide attempt is the most significant predictor of suicide. The courts have not opined on the recency of suicide attempt relevant to a liability claim. Clinically, a near-lethal suicide attempt within six months to a year has the most predictive value. Failure to question an inmate about history of past suicide attempts can lead to potential liability. While some inmates intentionally withhold the information, the prior records serve as the most reliable vehicle to get such information. To prevail in a lawsuit, a plaintiff must establish the decedent previously made near-lethal suicide attempt/s/

In Terry v. Rice (14), County officials went out of their way not to collect information from the prison where the decedent was transferred, presumably for “safekeeping.” In denying the summary judgment, the Court opined, “Going out of your way to avoid acquiring unwelcome knowledge is a species of intent. Being an ostrich involves a level of knowledge sufficient for a conviction of crimes requiring specific intent.”

In Mc Kee v. Turner, (!5) the treating psychiatrist was sued for failing to get prior jail records that indicated that the decedent had attempted suicide by hanging six weeks before he arrived at the prison. The dissenting judge opined, “McKee is distinguishable in one specific aspect, i.e., failure to obtain medical records.”

7 Diagnosis and Treatment Issues

Prisoners have claimed several diagnostic and treatment issues to support § 1983 claims.

a) Diagnosis of Mental illness

The diagnosis of a mental disorder or failure to diagnose per se does not support a claim of liability. While inmates diagnosed with depression, anxiety, and bipolar disorder have a high degree of suicidal propensity, unless indicators of suicide vulnerability accompany the diagnosis, the claim is not sustainable.

The Courts have held that displays of erratic behavior or signs of mental illness, without specific indicia of suicidal tendency, “do not rise to the level of a serious risk of suicide” and do not provide “the level of notice” required to trigger the deliberate indifference standard (16, 17)

b) Incorrect diagnosis

In Steele v. Choi (18), the Court concluded incorrect diagnosis or improper treatment does not support an Eighth Amendment claim. In affirming a summary judgment in favor of Dr. Choi, the 7th Circuit opined, “Estelle requires us to distinguish between `deliberate indifference to serious medical needs on the one hand, and `negligence’ in diagnosing or treating a medical condition.”

c) Intentional refusal to provide medical care.

Courts have acknowledged that intentionally refusing to respond to an inmate’s complaints, including repeated requests to see a mental health professional constituting deliberate indifference. Thus, to prevail, the plaintiff must establish the providers intentionally refused to provide medical care or denied access to a physician. Further, such refusal must cause the inmate undue suffering or threat of injury.

d) Delay in treatment

Courts have established that repeated delays in treatment of medical or dental conditions support a claim of deliberate medical indifference (19, 20). However, isolated delays or delays due to the natural course of events in a facility and administrative procedures, not an uncommon occurrence in a correctional setting, may not be actionable.

Delay of treatment claim depends on the length of delay, the nature of the medical need, and the reason for the delay (16) In Harris v Coweta County, (21), the Court held that such “a delay created a genuine issue of material fact about deliberate indifference.”

Delay in responding to repeated requests to see a mental health professional by a potentially suicidal inmate may result in a liability claim. In O’Quinn v. Lashbrook (22), the Court decided a claim of delayed treatment was meritorious.

e) Improper medication or modality of treatment

Improper medication treatment and medical supervision by the psychiatrist can support a claim of deliberate indifference if it can be proved such improper medication treatment cause suicidal ideation and serious injury resulting in death. Prisoners are not entitled to a specific prescription or modality of treatment if the choice of medication prescribed by the physician or the modality of treatment addresses his medical need.

f) Inadequate treatment

In Durmer V. O’Carroll, (23), the Court opined that all inadequate treatment provided to a prisoner could not be construed as deliberately indifferent. Instead, it can simply be “no more than mere negligence.” The Court further opined a failure or delay in providing prescribed treatment if deliberate and motivated by non-medical factors, a constitutional claim may be presented.

In Arenas v. GA Department Corrections, (24), the Court found that a failure to provide adequate treatment to a young inmate with a longstanding history of depression and bipolar disorder constituted deliberate indifference.

g) Inadequate monitoring of inmates in administrative segregation

Periodic reviews of inmate’s suitability to continued stay in administrative segregation is a standard procedure. Courts have recognized “substantial risk of psychological harm and decompensation posed by extended placement in segregation” including anxiety, panic, paranoia, depression, PTSD, psychosis, and disintegration of a basic sense of self-identity (25, 26)

8) Policy, staffing, and training

In many deliberate indifference lawsuits, counties face Monell claims related to suicide prevention policy, mental health and correctional staffing, and training.

Absence of suicide prevention policy

In White v. Watson (27), the Court opined that the absence of suicide prevention policy and lack of training and supervision were “the moving force behind the failure to protect the inmate from the known risk of suicide in the Jail.

Other Court decisions show that for a successful claim based on the absence of suicide prevention policy, evidence must be presented to show a pattern of suicide or suicide attempts.

2) Policy or custom causing or contributing risk of harm.

In Gibson v. County of Washoe, (28) the Ninth Circuit opined that County’s failure to respond to the decedent’s urgent need for medical attention was a direct result of “an affirmative County policy that was deliberately indifferent, under the Farmer standard, to this need.”

In Gates v. Cook (29), the Court noted multiple policies or practices that combine to deprive a prisoner of a “single, identifiable human need,” such as mental health care, can support a finding of Eighth Amendment liability.

3) Shortage of staff

In Bragg v. Dunn (30), the Court found persistent and severe mental-health and correctional staff shortages, combined with chronic and significant overcrowding, as the “overarching issues that permeate” the contributing factors of inadequate mental health care and suicide.

4) Failure to Train

Failure to train the staff focuses on the U.S. Supreme Court’s decision in City of Canton v. Harris (31). A County can be found deliberately indifferent if it fails to train officers to recognize suicide indicators, policy issues, monitoring procedures. Officers cannot be held liable for deliberate indifference “unless an inmate was so obviously mentally ill that the deputies, who had received no training regarding the diagnosis and treatment of mental illness, must have known that [he] was exhibiting symptoms of mental illness” (28)

Conclusion

The court decisions noted above provide valuable insights and directions to develop appropriate risk management strategies in jails and prisons.

***

Note: This article is abstracted from my book in preparation, titled, “Suicide in Jails and prisons: preventive and legal perspectives.

References

Comstock v. Mc Crary, [2001], 273 F.3d 693, 6th Cir

Williams v. Mehra [1999], 186F, 3d 686,690,6th Cir

Greason v. Kemp, (1990) 891 F.2d 829 (11t h Cir

Steele v. Shah, [1996], 87 F 3rd 1166, 11th Cir

Gordon v. Kidd, (1992) 971 F.2d 1087, 1095, 4th Cir

Conn v. City of Reno, 591 F.3d at 1105, 9th Cir

Freedman v. City of Allentown (1988) 853 F.2d 1111, 1117, 3d Cir

Woodward v. Myres, (2002) No. 00 C 6010, 99 C 0290, at *1, N.D. Ill.

Simmons v. Navajo County, (2010) 609 F.3d 1011, 1018, 9th Ci

Hott ex rel. Estate of Hott v. Hennepin County, (2001) 260 F3d 901, 8th Cir

Minix v. Canarecci, (2010) 597 F.3d 824, 833, 7th Cir

Broughton v. Premier Health Care Servs Inc, (2016), No. 15-4150, 6th Cir

Strickler v. McCord, (2004) 306 F. Supp. 2d 818, N.D. Ind

Terry v. Rice, (2003) CAUSE No. IP00-0600-C K/H, at *1, S.D. Ind

On December 20, 2017, the U.S House of Representatives and. Senate passed H.R. 1, “[a]n Act to provide for reconciliation pursuant to titles II and V of the concurrent resolution on the budget for fiscal year 2018” (referred to hereinafter as the “Tax Cuts and Jobs Act of 2017” or (“the TCJA”)), enacting the most sweeping tax reform bill in 30 years. Then-President Trump signed the TCJA into law on December 22, 2017. And as a result, most of the provisions of the TCJA became effective for tax years beginning after December 31, 2017 (January 1, 2018), and ending on December 31, 2025.

However, America now has a new president, Joe Biden, who during his campaign and subsequently after taking office has promised to bring an end to what he characterizes as the sweeping tax cuts in favor of corporations and high net worth individuals at the expense of the working-class Americans that the TCJA has wrought. And while world events have overtaken Biden’s young administration’s focus on bringing its version of tax reform to the forefront, I believe it might be prudent to use this lull in Congressional and Presidential focus on the Tax Code to reacquaint ourselves with the key provision of the TCJA and how they impact individual and business taxpayers.

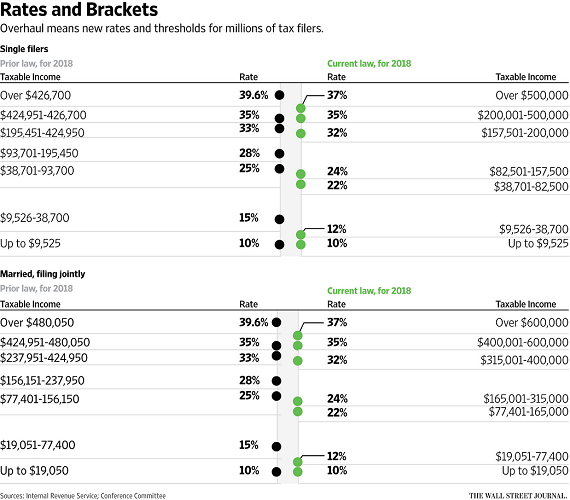

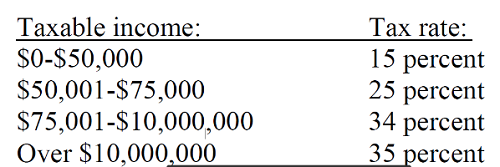

B. Changed Tax Rates and Brackets due to the TCJA of 2017

What follows is a chart comparing the tax rates and brackets for pre-TCJA-2018 and post-TCJA-2019 tax years.

Under the TCJA, the top tax rate drops from 39.6% to 37%, and it takes effect at $600,000 of taxable income for married couples rather than about $480,000 under the pre-TCJA regime. For single filers, the top rate takes effect at $500,000 rather than $426,700. The lowest rate remains 10%, which takes effect at the first dollar of taxable income. However, taxpayers may have more or less income before the 10% rate applies than they did in the past, due to changes to deductions, exemptions, and other provisions.

Let’s quantify the changes for a “typical” hypothetical taxpayer, Mary Jane:

In 2018 when filing her taxes for 2017, Mary Jane, a single lawyer-taxpayer with a taxable income of $100,000 paid $20,842.75 in taxes:($9,525 x 0.10 = $952.50) + ($29,175 x 0.15 = $4,376.25) + ($55,000 x 0.25 = $13,750.00) + ($6,300 x 0.28 = $1,764.00).

However, in 2019 when filing her taxes for 2018, as a result of the reduction of the tax rates and the expansion of the tax brackets, when filing for the 2018 tax year, Mary Jane, still single with a taxable income of $100,000 paid only $18,289.50 in taxes: ($9,525 x 0.10 = $952.50) + ($29,175 x 0.12 = $3,501.00) + ($43,800 x 0.22 = $9,636.00) + ($17,500 x 0.24 = $4,200.00).

C. Key Deduction/Exemption Changes Bought on by the TCJA

This section highlights the key changes the TCJA of made applicable to individuals. Changes affecting businesses, including provisions affecting corporations versus pass-through entities, such as proprietorships, partnerships, S corporations, and their owners, are addressed in Part E., below.

While the TCJA made a number of important changes to the taxation of individuals, many of these provisions, unless extended by Congress, will sunset in tax years beginning after December 31, 2025 (January 1, 2026), at which time the rules under pre-TCJA law will spring back into effect.

1. Elimination of Taxpayer Personal Exemptions/ Increase in the Standard Deductions

For many taxpayers, especially those with several dependent children, the TCJA’s most sweeping change was the increase in the standard deductions and the repeal of all personal exemptions. The TCJA raised the 2018 standard deduction to $24,000 per married couple and $12,000 for singles, compared with $13,000 and $6,500, respectively, under prior law.

As a result, the number of filers who itemized for 2018 was expected to, and did, drop by more than half—from nearly 47 million to about 19 million out of about 150 million expected tax returns, according to the Tax Policy Center.

As a result of the change, taxpayers can no longer claim a personal exemption deduction for themselves, their spouse or any of their dependents. Each personal exemption in 2017 provided a $4,050 tax deduction. This allowed a family of four to deduct a total of $16,200 in addition to a standard deduction of $13,000, itemized deductions and any adjustments to income. The loss of this personal exemption deduction greatly reduced the tax benefit of the increased standard deduction for taxpayers with large families.

To make up for the loss of this deduction, the child tax credit for qualifying children under the age of 17 was increased by $1,000 and made available to more taxpayers. Additionally, the TCJA created a new $500 credit for all other dependents, though there is no credit for the taxpayer and her spouse.

2. Elimination of Alimony (Paid) Deduction and Alimony Received (Inclusion)

For divorce decrees or separation agreement executed after December 31, 2018, any alimony paid was no longer a deductible expense for the payer. And any alimony received no longer needed to be included in the taxable income of the recipient. It is important to note that this new rule did not affect tax year 2018 returns or anyone who at the time of enactment was then paying or receiving alimony. Taxpayers who divorced before December 31, 2018 continued to be able to deduct and/or are required to report alimony payments as income.

3. Elimination of the Nonmilitary Job-related Moving Expenses Deduction

Under the TCJA, job-related moving expenses paid by an employee lost their deductibility. Only active-duty members of the armed forces who move due to a military order can claim that activity as an adjustment to income. As of the new law, employer-to-employee payments of non-military moving expenses became income that must be included in the employee’s taxable wages, tips, and other compensation reported on a W-2.

4. Limits on Mortgage Interest Deductions for Acquisition Debt and Elimination of the Home Equity Loan Interest Deduction

Under the TCJA taxpayers could continue to claim an itemized deduction for their home mortgage interest on acquisition debt — that is, debt secured by the home and used to buy, build or substantially improve it — up to $750,000 in principal ($375,000 if married and filing separately) on home purchases made after December 15, 2017.

Interest on then-existing acquisition debt of up to $1 million in principal for home purchases made prior to December 16, 2017 was “grandfathered” and remains deductible. The higher $1 million principal limit also applies to acquisition debt incurred before December 16, 2017 that is subsequently refinanced.

Home equity interest – interest on mortgage debt to pay for anything other than to buy, build or substantially improve a residence – became no longer deductible under the TCJA. Additionally, existing home equity debt was not grandfathered.

As a result of the TCJA it has become more important than ever for homeowners who can itemize to keep separate track of acquisition debt and home equity debt going back to the original purchase of their residences.

5. Elimination of the Casualty Loss Deduction

Only a taxpayer who suffers a personal casualty loss from a disaster declared by the presidentwill be able to claim a personal casualty loss as an itemized deduction. Casualty losses are losses sustained by a taxpayer that are not connected with a trade or business or otherwise entered into for profit. They include property losses arising from fire, storm, shipwreck, or other casualty, or from theft.

6. Elimination of the Employee Business Expenses Deduction

Pursuant to the TCJA, none of the previously allowed miscellaneous expenses that were subject to the 2%-of-AGI exclusion remain deductible on Schedule A. Employee business expenses that had not been reimbursed by the taxpayer’s employer were the most prominent deductible items in this category.

Additionally, the TCJA eliminated employee-taxpayers’ ability to deduct business meals, travel and entertainment from their taxes. The eliminated deductions included using a car for business as well as job-related education, job-seeking costs, a qualified home office, union and professional dues and assessments, work clothes and work supplies.

7. Elimination of Investment Expenses Deductions

Investment expense recapture was also eliminated under the TCJA, making it no longer deductible as a miscellaneous expense on Schedule A. The eliminated expenses include custodial and maintenance fees for investment and retirement accounts, fees for collecting dividends and interest, fees paid to investment advisers, the cost of investment media and services, and safe deposit box rental fees. Investment interest remains deductible as interest on Schedule A, subject to the limitations of IRS form 4952.

8. Tax Preparation Fees Deduction

Expenses paid or incurred by an individual in connection with the determination, collection, or refund of any tax are no longer deductible on Schedule A pursuant to the TCJA, no matter which level of government is presiding over the taxation or even what the tax is levied upon.

9. Elimination of Certain Legal Fees Paid on an Award, Judgment or Settlement Deduction

The TCJA also changed the nature and structure of financial agreements between counsel and our clients. For example a legal award, judgment or settlement for personal physical injuries or physical sickness is tax exempt. So, the related legal fees are not deductible since that income is not taxable. Also, in the wake of the “#metoo” and “Time’sUp” movements, there is no deduction for sexual harassment or abuse settlements if the settlement includes a non-disclosure agreement.

Legal fees related to an award, judgment or settlement of claims of unlawful discrimination are deducted as an adjustment to income on the 1040 form, reducing adjusted gross income.

However, all other Legal fees related to all other taxable awards, judgments or settlements, which were previously allowable as miscellaneous expenses on Schedule A, are no longer deductible on the 1040. For example, if a taxpayer is awarded a settlement of $100,000 and her attorney receives $30,000 of it, the taxpayer must pay federal income tax on the entire $100,000 even though she only received $70,000.

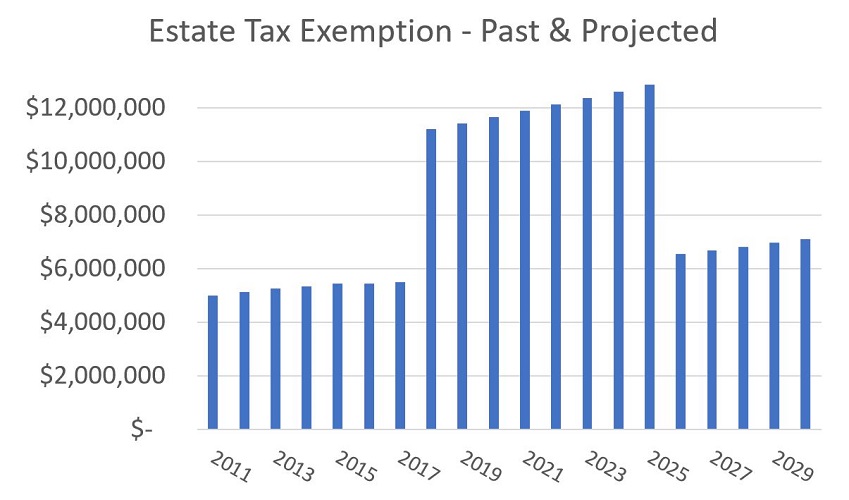

10. Doubling of the Estate and Generation Skipping Tax Exemption to $11,400,000 ($22,800,000 for married couples)

The TCJA doubled the estate and generation-skipping tax exemption to $11,400,000 ($22,800,000 for married couples). Additionally, the step-up in basis is retained at death. As can be seen from the following graph, the enhancement sunsets at December 31, 2025.

Illustration by: Keebler Tax & Wealth Education, Inc.

11. New Flexibility in Education Provisions

Post TCJA, Section 529 Plans allow the distributions of up to $10,000 for “qualified expenses” for elementary school and high school, and starting in 2018, the forgiveness of student loan debt will not be taxable income to the student on account of the student’s death or total disability.

12. New Flexibility for ABLE Accounts

The TCJA also allows for increases in contribution limits in certain circumstances and allows for rollovers from 529 accounts to ABLE accounts.

D. State and Local Tax (“SALT”) Issues

“The U.S. Supreme Court’s ruling in South Dakota v. Wayfair Inc., No. 17-494 (U.S. 6/21/18), coupled with the passage of the TCJA, has had the greatest impact on SALT practice in decades, positioning SALT issues to be a one of the leading consideration in the overall tax landscape in the 2019 tax return preparation season and beyond While the reverberation of tax legislation can sometimes take months or longer to take hold, Wayfair and the TCJA began to make waves across the country in just a matter of weeks. For taxpayers and tax professionals this consequence continues to mean that SALT’s influence is now greater than ever, drawing more attention to the key role indirect taxes play in a taxpayer’s comprehensive tax strategy.” [1]

1. The TCJA’s SALT Deduction Limitations

Under TCJA, the SALT deduction was limited to only $10,000.00 per household as to an individual or married filing jointly taxpayer. This limitation has proven to be a handicap for many taxpayers, especially those who are homeowners in high home value states such as California and New York; taxpayers who have traditionally been able to take substantial itemized deductions for both the interest paid on their mortgages and the property taxes paid to their county tax collectors.

However, state, local, and foreign property taxes and state and local sales taxes continued to be allowed as a deduction when paid or accrued in carrying on a trade or business, or an activity described in section 212 (relating to expenses for the production of income).

2. The Impact of Wayfair on the taxation of e-commerce taxpayers.

Wayfair, which held that states can mandate that out-of-state retailers collect sales taxes from in-state customers, even if the retailers have no physical presence in the state. As such, “Wayfair overturned 26 years of precedent (see Quill Corp. v. North Dakota, 504 U.S. 298 (1992)) by changing the nexus landscape from a physical presence to more of an economic influence considering how companies do business in today’s digital climate. Over the past two decades it had been challenging for states to meet budget requirements, and some would assert that this problem was attributed to out-of-state retailers being able to skirt their sales tax responsibilities thanks to the precedent from Quill, which was decided in a less digital world.

“Once the opinion was handed down in Wayfair, it did not take long for states to act and enforce sales tax requirements on out-of-state sellers selling goods and services into their jurisdictions. Before this landmark decision, just 20 states had some sort of economic nexus standard on the books or in the works. Within eight weeks after it, that number was up to 30 plus. The case has also opened the door for states without a sales tax to reconsider implementing one, as e-commerce becomes the norm.

“On the taxpayer side, misconceptions exist that because remote sellers were not charging sales tax on their goods, those transactions were tax-exempt. In reality, those transactions were supposed to be reported on use tax returns, but very few consumers complied with these obligations. Going forward, individuals will likely have to start paying sales tax on more of their out-of-state purchases, which can be seen as leveling the playing field between e-commerce and brick-and-mortar retailers.”[2]

[1] Brawdy, Why SALT will take center stage next to tax reform in 2019, The Tax Adviser (Dec 1, 2018)

E. Overview of the TCJA’s Reduction of the Top Corporate Tax Rate from 35% to a Flat 21% Rate and Section 199A, the New 20-percent Deduction for Pass-through Businesses Pursuant to Section 199A of the Internal Revenue Code

1. Corporate and Small Business Tax Rates Reduction

Under the pre-TCJA law, “the highest corporate income tax rate was 35% and the highest rate of tax on qualified dividends received by an individual was 23.8 percent (20% plus the 3.8% tax on net investment income). As a result, under pre-TCJA law, the overall effective rate on corporate income distributed to individual shareholders was 50.47 (35% taxable income plus 15.47% (65% of taxable income times 23.8%)).” [1]

The TCJA eliminated the graduated income tax with a top rate of 35% and replace it with a flat 21% corporate income tax rate beginning in the 2018 tax year.

Corporate Tax Rate

2017

2018

21% Flat rate

According to a joint analysis from the CongressionalBudget Office (“CBO”) and the Joint Committee on Taxation (“JCT”), the reduction will reduce revenue by $1.65 trillion over a decade. These corporate tax changes are permanent, while many of themajor individual provisions, including changes for pass-through businesses, discussed below, will sunsetfor tax years beginning after December 31, 2025.

“Also, prior to the TCJA, sole proprietorships and owners of pass-through entities were subject to a maximum marginal rate of 43.4%, (39.6% plus 3.8% if the income was not subject to self-employment (“SE”) tax). Beginning on January 1, 2018, and ending on December 31, 2015, the highest individual rate is now 37% resulting in an effective rate of 40.8% when the net investment income tax applies.

“With the corporate income tax rate now a flat 21% and the corporate alternate minimum tax (“AMT”) repealed, a C corporation distributing all of its after tax profits as dividends to individual shareholders in the highest tax bracket results in a maximum effective rate of 39.8%, (21% of taxable income, plus 79% of taxable income times 23.8%). Thus, the reduction in corporate and individual tax rates after December 31, 2017 reduces the highest marginal effective rate on business income from 50.47% to 39.8% for a C corporation distributing its after-tax profit and from 43.4% to 40.8% for pass-through entities.”[2]

2. An Overview of the TCJA’s Section 199A’s Qualified Business Income Deduction

After all the math is done, Section 199A of the TCJA .grants an eligible business-owner-taxpayer other than a corporation a deduction equal to 20% of the taxpayer’s qualified business income, subject to deduction phase-outs and limitations phase-ins that are dependent upon the type of business the taxpayer is engaged in.

For example, for business owners with taxable incomes in excess of $207,000 ($415,000 in the case of taxpayers married filing jointly), the 20% deduction is phased-out, such that no deduction is allowed against income earned in a “specified service trade or business,” (“SSTB”).

Specified Service Trade or Business

Health

Law

Accounting

Actuarial science

Performing arts

Consulting

Athletics

Financial services

Brokerage services

Investing and investment management

Services in trading

Services in dealing securities, commodities, and partnership interests

Any trade or business where the principal asset of such trade or business is the reputation or skill of 1 or more of its employees or owners

On the other hand, at these same income levels, the deduction against income earned in an eligible business, a non-SSTB, is limited to the greater of:

50% of the taxpayer’s share of the W-2 wages with respect to the qualified trade or business, or

The sum of 25% of the taxpayer’s share of the W-2 wages with respect to the qualified trade or business, plus 2.5% of the taxpayer’s share of the unadjusted basis immediately after acquisition of all qualified property.

199A’s Business Classifications, Deductions and Limitations

Non-Service or Non SSTB Service Business

SSTB Service Business

Taxable income less than $315,000 (MFJ 2018)

20% deduction

20% deduction

Taxable income greater than $315,000 but less than $415,000

Limitation phased-in

Deduction phased-out

Taxable income greater than $415,000 (MFJ 2018)

Wage/Capital Testing

No deduction

Illustration by: Keebler Tax & Wealth Education, Inc.

Once the taxpayer’s 20% deduction is computed and limited, as appropriate, it is added to the second deduction offered under Section 199A; a deduction for 20% of the taxpayer’s qualified REIT dividends and publicly traded partnership (PTP) income for the year. These two deductions are truly separate and distinct. For example, if a taxpayer has a net loss from her pass-through businesses, it does not preclude the taxpayer’s ability to claim a deduction of 20% of REIT dividends and PTP income. Likewise, if a taxpayer’s sum of REIT dividends and PTP income is a loss, it does not reduce the taxpayer’s pass-through deduction.